Before you dive into the article, pay attention to the fact thatthe fact that none of theis financial advice, please do your own research to make a more informed decision.

The first RMM-based product launched on April 20, 2022.

⁃ CFMM (Constant Function Market Makers) is a classic AMM model used in Uniswap, Balancer, etc.

⁃ RMM (Replicating Market Makers) - a rethinking of CFMM: CFMM, the payment structure within which replicates/duplicates other instruments (in this case, options).

⁃ Primitive is the first project to use RMM.

The main message of the creators of RMM and Primitive:

⁃ all applications in DeFi have one criticalperiod - these are oracles. Oracles are unsafe, expensive, and unnecessarily complicate application design. RMM eliminates the need to use external oracles;

⁃ RMM is more efficient compared to classical AMM and SSOV.

RMM-01 (Primitive's first product) in terms ofthe user will be an AMM, but at the same time it will be more convenient and efficient for liquidity providers (who, when providing liquidity, will essentially simultaneously sell call options), and will also attract a new category of users - arbitrageurs. In addition, according to the creators of RMM, it is also an infrastructure for creating more complex structured products (binary options, for example).

Main participants of RMM:

⁃ traders: swap tokens;

⁃ liquidity providers: supply liquidity + sell call options;

⁃ arbitrators:those who rebalance protocol reserves until the payment structure set by the creators of the pools is achieved. The design of pools is such that arbitrageurs make a profit only when they rebalance pools closer to a given structure: in other words, every “correct” swap by an arbitrageur (and only such a swap will be profitable for him) brings the payout to the liquidity provider closer to the payout he would have received in the form of a premium for selling a call option - that is, pools and payments in them seem to replicate/duplicate the “behavior” of the option. In fact, arbitrage traders take the place of oracles in RMM-01, acting as “final price validators”.

“RMM-01 is positioned as “Covered Call”CFMM”, which estimates the value of assets in pools based on their price, volatility and time period.” That is, it is something like AMM for covered call options (but not exactly that). That is, the liquidity provider, by providing notional ETH, not only provides liquidity, but also uses ETH to back the call option it sold. That is, the ETH provided provides call option + liquidity for swaps. And instead of a premium for writing options, liquidity providers receive commissions from the pool (from traders and arbitrageurs).

Compared to AMM to RMM:

⁃ liquidity providers can choose fromat what point are they ready to bear IL, and also determine the pricing strategy (that is, IL will begin only after reaching the strike price - a liquidity provider can, with an ETH price of $3k, indicate a willingness to bear IL risks only from $4k);

⁃ the amount of commissions depends on time and volatility;

⁃ some other differences, the essence of which I did not quite understand, such as “RMM curves concentrate liquidity closer to the expiration date, while Uniswap has concentrated liquidity fixed.”

Compared to covered call options in RMM:

⁃ external oracles are not used;

⁃ no counterparty is required;

⁃ at any time, tokens of liquidity providers can be exchanged for the underlying asset + in this regard, they can be used in defi as collateral.

And yes, on exit (after the expiration datepool actions) you will receive (1) 100% in stablecoins if the price of a non-stablecoin is above the strike, (2) 100% in a non-stablecoin if the price of a non-stablecoin is below the strike.

What can you do on the site?

⁃ provide liquidity - you give two tokens(one of them is a stablecoin), you choose the strike price (here we not only provide liquidity, but also sell call options), the implied volatility level (the expected volatility of the asset before the pool expiration date), the pool expiration date and gamma (determines the size of commissions) ;

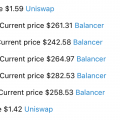

⁃ swap tokens;

⁃ use the received LP tokens as collateral for a loan (apparently sometime in the future);

⁃ create vaults (automated strategies) on top of RMM pools.

In developing:

⁃ tokenized theta;

⁃ vanilla options;

⁃ binary options.

Read this:

Zavyalov Ilya Nikolaevich about cross-chain

Zavyalov Ilya Nikolaevich about cross-chain

Zavyalov Ilya Nikolaevich about metagovernance in cryptocurrency.

Zavyalov Ilya Nikolaevich about metagovernance in cryptocurrency.

Trading signals! | Zavyalov Ilya Nikolaevich about BTC/USDT 09.29.23

Trading signals! | Zavyalov Ilya Nikolaevich about BTC/USDT 09.29.23

Trading signals! | Zavyalov Ilya Nikolaevich about BTC/USDT 09/28/23

Trading signals! | Zavyalov Ilya Nikolaevich about BTC/USDT 09/28/23

Bitcoin is a huge predominance of call options.

Bitcoin is a huge predominance of call options.

DeFi and crypto farming, how not to burn yourself?

DeFi and crypto farming, how not to burn yourself?